"CompLab" is the blog on competitiveness and growth coordinated by Carlo Altomonte

In Italy’s public debate on the PNRR (National Plan for Recovery and Resilience, the Italian implementation of Next Generation EU), a misleading narrative has now taken hold: that of the Plan’s “success” or “failure.” This simplification risks obscuring the most relevant issue for the Italian economy: not whether the PNRR has worked, but what it has actually produced and why this has not yet translated into sustained growth.

To try to answer this question, it is worth starting from what we know and what the data confirm with some clarity.

Italy’s Plan is now among the most advanced in Europe in terms of implementation: more than 85% of the resources have already been received (the ninth “installment” arrived at the end of April), and by the end of 2025 around 110 billion euros had formally been spent. The administrative machinery has activated hundreds of thousands of projects, and a significant share of interventions, more than 70%, has already been completed.

But the most important figure is not merely administrative. It is macroeconomic. The Bank of Italy, in its commentary report on the government’s Public Finance Document a few days ago, certifies that in recent years, partly thanks to the PNRR, public investment has reached levels not seen since the beginning of the century: in 2025 it amounted to 3.8% of GDP.

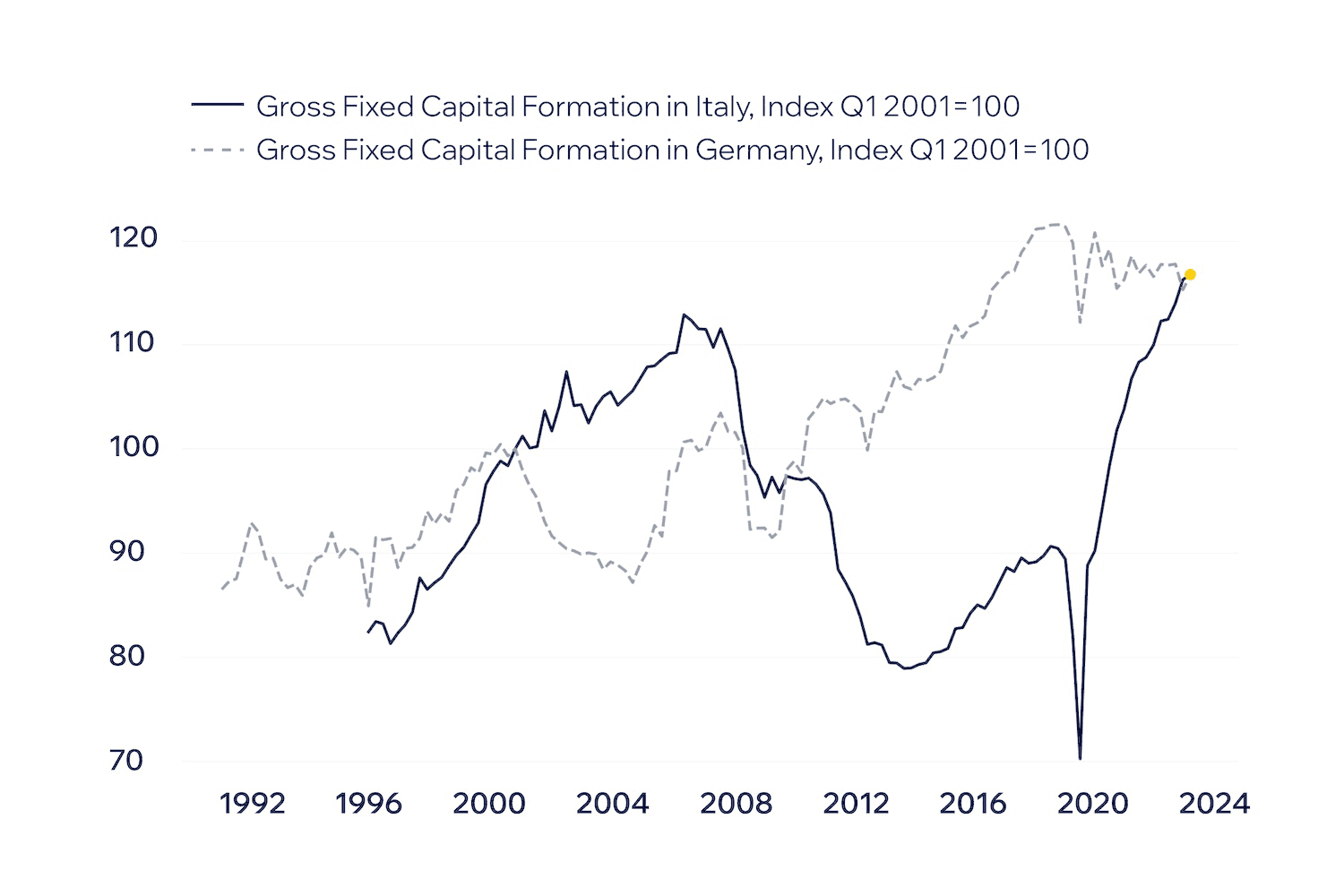

After all, it is enough to look at the chart below: it shows the evolution of total investment (Gross Fixed Capital Formation) in Italy and Germany, both indexed to 100 in 2001 (source: OECD).

A tale of two countries

It shows that, after the financial crisis and the pandemic, Italy accumulated a gap of 40 points (!) compared with Germany in terms of investment. But it also shows that between 2021 and 2024 this gap was completely closed (!!).

This is exactly why the Plan was conceived: to close the physical and infrastructure capital deficit that Italy had accumulated after the financial crisis and the pandemic. From this point of view, the PNRR has therefore achieved its main objective: reactivating investment dynamics.

And yet growth remains weak. The most recent forecasts point to GDP rising by around 0.6% in 2026 and 0.5% in 2027. This is where the debate should change direction. The issue is no longer the quantity of investment, but its ability to turn into growth.

The PNRR was, by design, a supply-side policy instrument: it increased the stock of public capital and encouraged private capital. But growth depends on at least three additional conditions:

- The quality of the capital created: not all investments have the same impact on productivity. The recent reallocation of resources — cutting less mature projects and strengthening incentives for businesses, such as tax credits for the SEZ — moves precisely in this direction. But the question remains open: how much of this capital is truly “transformative”?

- The institutional context: the Bank of Italy itself stresses that growth requires reforms that foster innovation and productivity. Without improvements in the public administration, justice system, and competition, even an increase in investment risks producing diminishing returns. Here the PNRR has produced results, from eliminating the backlog of pre-2019 civil justice cases to reducing public administration authorization times, but has it done enough?

- The functioning of the labor market: if capital grows but labor does not adapt — in terms of skills, mobility, and incentives — the result is stagnant productivity. This is a structural problem that the PNRR has addressed only partially.

There is also an element that is systematically overlooked in the debate: aggregate demand. In recent years, Italy’s macroeconomic picture has been characterized by tax pressure that has remained consistently high (above 43% of GDP) and by real wages which, according to the 2025 ISTAT Annual Report, lost 10.5% of their purchasing power between 2019 and 2024 (!). Add to this a worsening climate of household confidence, also as a result of geopolitical uncertainty.

It is clear that, under these conditions, even a strong investment impulse risks failing to translate into sustained growth in consumption and therefore in GDP. The result, then, is THAT supply is probably improving, but demand remains weak.

So, what should be done? Fortunately, the PNRR does not really end in 2026. The introduction of financial instruments — around 24 billion euros entrusted to entities such as CDP and Invitalia — makes it possible to extend the effects of the Plan for at least two more years. These resources will also be joined by those from cohesion policy, which has likewise been reshaped with an approach based on objectives and targets similar to that of the PNRR. So although many resources have already been committed, they will produce economic effects in the following years. We must therefore make an effort to use this “bridge” to build stronger growth over the rest of the decade.

In conclusion, framing the problem of Italian growth in terms of whether or not the PNRR has “failed” is a very partial and distorting approach. Rather, the PNRR is the test that shows where the real problems behind our country’s lack of growth lie. With the PNRR, we have been able to mobilize resources, close the investment gap, and improve administrative capacity, at least in part. But we have also realized that all this is not enough. Because growth does not depend only on capital. It depends on how an economic system as a whole — institutions, labor, businesses, households — manages to use it. And this is exactly where the debate on the country’s growth and competitiveness should shift. Not the PNRR itself, but what is missing for it to truly work.